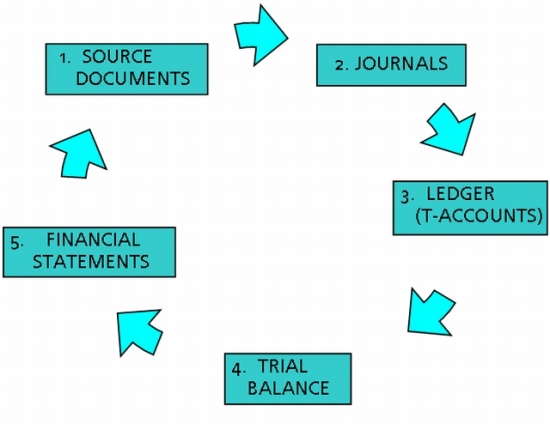

The relationship among journals, ledgers, trial balances, and financial statements are important procedures in the accounting cycle we learned. First, the transaction occurs which is then recorded into the journal of when the transaction had taken place. Then the information from the journal entries are transferred to the ledgers. Then like so, the information in ledgers transfer to the trial balances as it it prepared and then converted into a work sheet to create financial statements such as income statements along with balance sheets.